ibe121

Member

- Joined

- Jul 28, 2023

- Threads

- 0

- Messages

- 6

- Reaction score

- 11

- Location

- California

- Car(s)

- 2013 Mazda CX-5

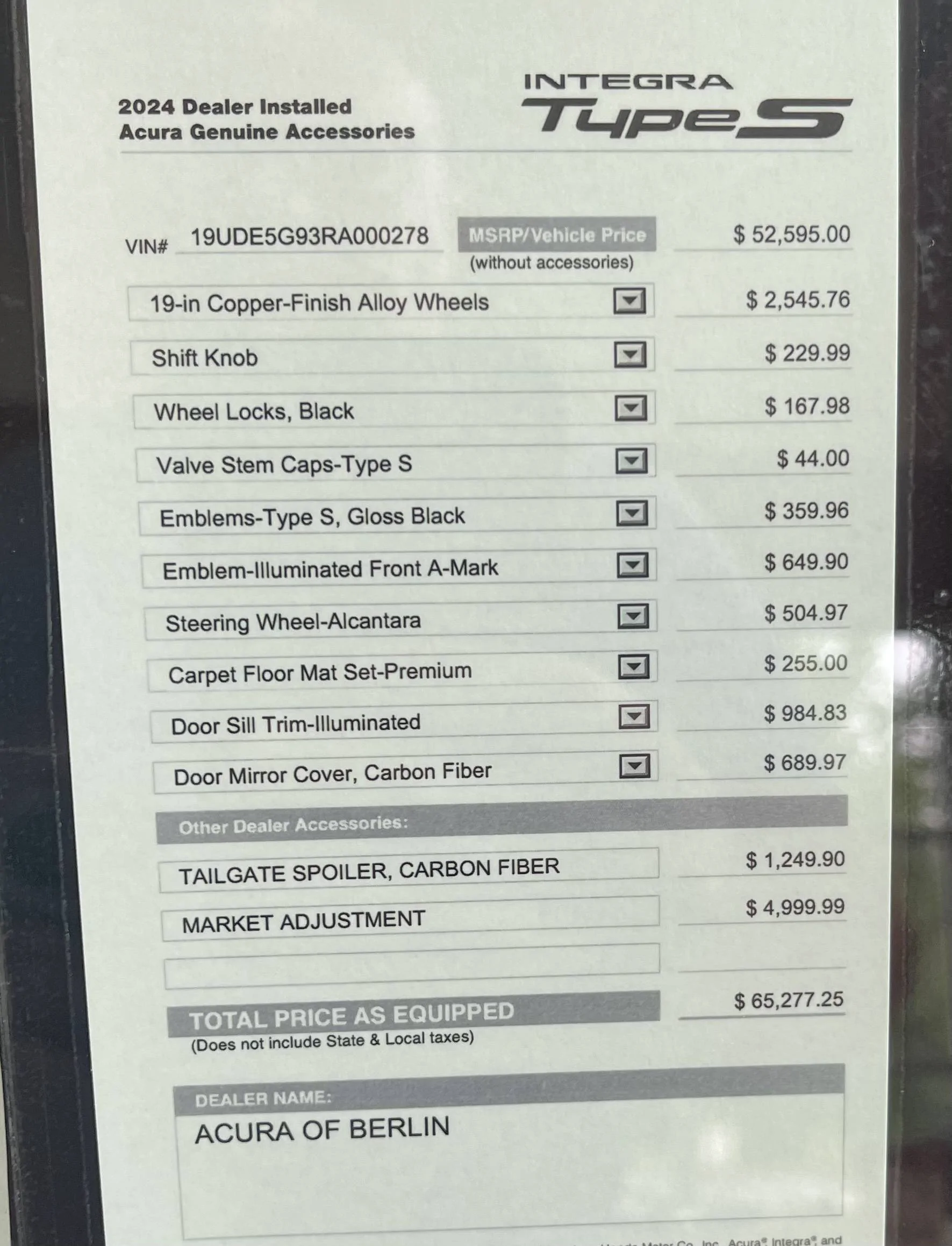

Last week they just quoted me $10k for the ADM. Marin quoted me $7,500k and the guy at Hopkins said they'd match Marin if I could prove it. So, I sent him the screenshot of the email from Marin and he said they'd match. Interesting to see them go from $19k to $7.5k in a matter of months. Still sucks to be dealing with ADM's but I guess that's progress.Hopkins Acura of Redwood City $19k adm. they trying to undercut the $20k dealers. Haha…..Man this sucks!

Sponsored